Interim IRS OZ Guidance

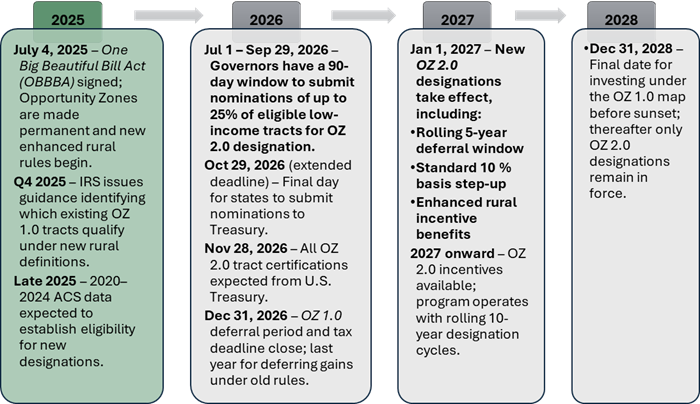

With the transition from the original Opportunity Zone program (OZ 1.0) to the new OZ 2.0 regime fast approaching on January 1, 2027, the IRS recently dropped Notice 2026-40.

Driven by the One Big Beautiful Bill Act (OBBBA), this interim guidance clarifies the rules of the road for the great OZ handoff. For investors and developers, it is a classic "good news, bad news" scenario.

Here is what you need to know to protect your capital and navigate the transition.

The Door Closes: No Re-Deferring Your 2026 Tax Bill

For years, a popular tax-planning hope circulated: when the original OZ 1.0 deferred gains finally trigger on December 31, 2026, could investors simply roll those recognized gains into a new QOF and kick their deferred capital gain tax further down the road?

The IRS has now officially and definitively shut that door.

The Ruling: Capital gains originally deferred under OZ 1.0 that are recognized on December 31, 2026, cannot be reinvested into another QOF for a second round of deferral.

What this means for you:

- A Real Tax Liability: You must prepare to pay the tax on those original deferred gains when filing your 2026 tax return (or extension) in April 2027.

- Active Planning Required: Work with your tax advisor now to explore mitigation strategies—such as tax-loss harvesting, charitable giving, or maximizing passive losses—before the end of the year.

- Your 10-Year Benefit is Safe: Paying the tax bill in 2026 does not kill your long-term benefits. If you keep your money in your current QOF for the required 10-year hold, your eventual exit remains 100% tax-free.

The Door Opens: Bridging OZ 1.0 Tracts into the OZ 2.0 Era

While the IRS closed the door on re-deferrals, they opened a highly anticipated pathway for deploying new capital into existing OZ 1.0 designated tracts.

If you want to invest new capital gains into an existing OZ 1.0 project and still secure the full suite of OZ 2.0 tax benefits, the project must meet three strict requirements by the December 31, 2026, deadline:

- Written WCSH Plan: The project must operate under a valid, written Working Capital Safe Harbor (WCSH) plan adopted on or before December 31, 2026.

- The 10% Capital Test: At least 10% of the project's total estimated working capital must be physically received at the operating business level (the QOZB) by the deadline.

- The 5% Commitment Test: At least 5% of the total estimated working capital must be expended or committed under binding written contracts by the deadline.

If a project fails to clear these three hurdles by December 31, 2026, it will be frozen out of the new post-2026 OZ 2.0 tax benefits that take effect January 1, 2027

The Post-2026 Playbook: A Brand-New 10-Year Cycle

For capital deployed on or after January 1, 2027, we enter the official OZ 2.0 era. The rules of engagement are shifting from a single calendar deadline to a clean, rolling timeline:

| Feature | OZ 2.0 Rules (Post-2026) |

| Deferral Timeline | Flat five-year deferral from your initial investment date. |

| Standard Step-Up | A 10% basis step-up once you cross the five-year mark. |

| Rural Benefit | A 30% basis step-up if investing in a Qualified Rural Opportunity Fund. Promised Land OZ is targeting a fully compliant Qualified Rural Opportunity Zone Fund (QROF) to take advantage of this valuable incentive. |

| Compliance Runway | Expired OZ 1.0 tracts can be treated as qualified zones for compliance testing through December 31, 2047. |

Additionally, don't worry if you harvest capital gains late in 2026. The IRS confirmed that pre-2027 gains can still qualify for the OZ 2.0 framework as long as they are deployed within their standard 180-day window, even if that window extends into 2027. That eligibility window started on July 9, 2026, assuming a January 1, 2027, investment date.

The Bottom Line

The OZ 2.0 rules of the road are settling, and the OZ roadmap is being redrawn. States are currently going through their determination process to nominate new OZ 2.0 designated tracts. Eligible census tracts are 25% fewer due tighter low-income community determination factors starting in 2027.

In addition, the window to act on projects in existing OZ 1.0 designated tracts is rapidly closing. Proactive OZ fund sponsors are busy using the next five-months to identify viable OZ 1.0 projects, align safe harbor plans to achieve requisite capital raising and commitment thresholds, and preparing for the OZ 2.0 starting gun on January 1, 2027.

Author: Dylan Gardner and John Heneghan

Observations from Mid‑South ASFMRA

It was a privilege for the Promised Land Opportunity Zone team to join the 2026 American Society of Farm Managers and Rural Appraisers (ASFMRA) Mid-South Chapter meeting in Starkville, Mississippi, earlier this month, sharing the exciting potential of rural Opportunity Zone (OZ) investment, alongside farm managers, appraisers, lenders, and Mississippi State University Extension economists. One message came through clearly: this past year and next are going to be challenging for many American farmers. Yet throughout two days of formal and informal conversations with attendees, a message of resilience also became quite clear: we’ve been here before, and we‘ll get through this downturn as well

American agriculture is a cyclical business in an often volatile world, yet it has remained one of the most durable, long-term engines of the U.S. economy. That resilience has always rested on two pillars: the ingenuity of American farmers and the enduring value of productive land and the food, feed, and fuel it produces.

What We Heard in Starkville

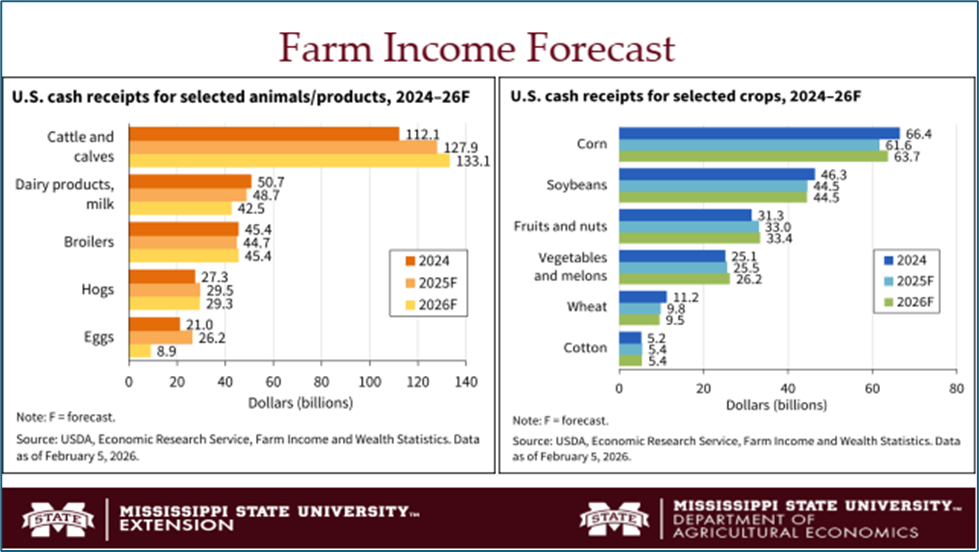

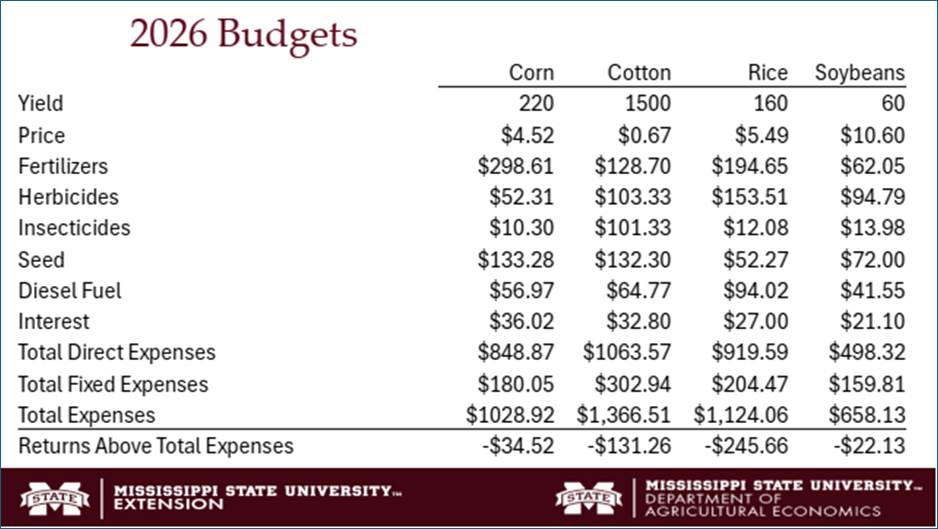

MSU Extension’s market and finance updates clearly identified that net farm income continues to be under pressure, with lower cash receipts and higher expenses squeezing margins across major Mid-South crops.

This pressure extends directly from the combination of lower commodity prices combined with consistently increasing costs of farm inputs eroding farm profitability as reflected in the pro forma below:

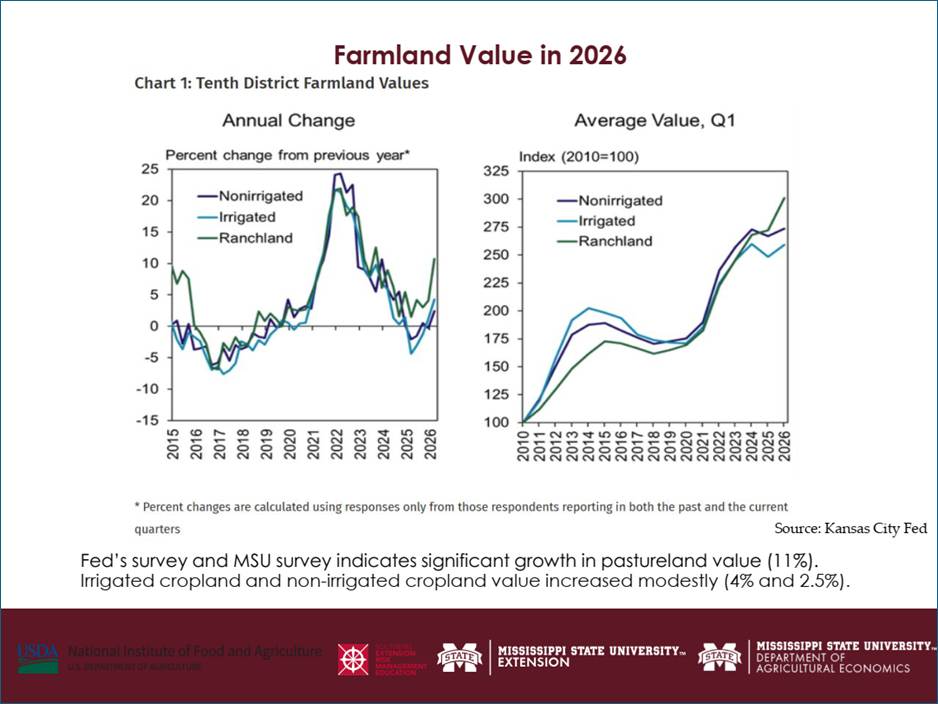

On the other hand, the farmland market data continues to tell its enduring story of resilience and stability, even when farm incomes are under pressure. Though cash rents for cropland have moderated slightly, farmland values in Mississippi have held up with projections of modest increases for 2026:

Many of these economic pressures on the farming economy are being driven by broader national and global economic and political forces outside of the agricultural sector’s control. These disruptive periods happen from time to time and are often short to intermediate term impacts from supply and demand imbalances for crop inputs and commodity prices. Despite these present challenges, the tenor of the group remained one of resilience, rather than resignation. A shared confidence permeated the room that, through disciplined operational execution, prudent financial management, and bushels of persistence and patience, these cyclical headwinds will once again be managed.

Promised Land: Shared Confidence in the Resiliency of American Agriculture

Promised Land shares that confidence in the enduring resiliency of American agriculture and in the people who operate within it. The Mid-South ASFMRA Starkville meeting offered a timely opportunity to underscore our belief that high-quality farmland, operated by capable tenants supported by patient, impact-oriented capital, can deliver on the promise of OZs —for investors and rural communities alike.

We presented our educational materials and investment approach for rural OZs to these professionals who see the market up close. Our presentation, “Opportunity Zone 2.0 Goes Rural,” outlined how the next chapter of the OZ program strengthens the toolkit for investing in rural America—through permanent OZ authorization, higher capital gain deferral basis step‑up for rural OZs (30% versus 10% for non-rural), lower substantial‑improvement thresholds for rural OZs (50% versus 100% for non-rural), and an expanded tax benefits for investments in production and processing assets under the One Big Beautiful Bill. For OZ investors, that means more ways to align impact capital with high‑quality farmland and essential agricultural infrastructure while capturing meaningful OZ tax benefits.

Confidence in American agriculture is grounded in the ag sector’s long‑term results rather than the economic machinations of any single crop year. The 2026 Mid‑South ASFMRA meeting underscored that, even in this more difficult part of the agricultural cycle, confidence in the resiliency of the American agricultural sector remains well placed. Promised Land is grateful to the Mid‑South ASFMRA Chapter for the opportunity to engage its membership, deepen their awareness of rural OZs, and reinforce Promised Land’s role in delivering purposeful results for rural American communities that have fallen behind economically from the rest of this great Nation.

The team at Promised Land wishes you all a safe celebration of America’s 250 years of Independence on the 4th of July.

Author: Mark Jablonski

Take It Easy released in 1972 was the debut single from their self-titled album, Eagles. This song is perhaps the most iconic tune about rural America among many. The song was written by Jackson Browne and Glenn Frey, inspired by the feelings of a road trip down Main Street America – Route 66. For far too long, rural America has been viewed through the reductive lens of flyover and drive through country. In this short piece, we’d like to introduce you to some of the street corners of rural Opportunity Zone investing.

A landmark August 2025 report from the McKinsey Institute for Economic Mobility challenges this “nothing to see here, move along narrative”, revealing an often stunningly diverse economic landscape that contributes $2.7 trillion to U.S. gross domestic product (GDP) (nearly 10%). The report, "Small towns, massive opportunity," identifies a critical need for targeted investment to unlock the potential of rural America’s 46 million residents.

The McKinsey Thesis: A Landscape of Distinct Archetypes

McKinsey’s data-driven analysis categorizes rural America into six distinct "archetypes," each with unique economic drivers and investment profiles. Three archetypes stand out as particularly ripe for growth:

- Agricultural Powerhouses: These communities drive the nation's food security, with agriculture accounting for 20% or more of their GDP. They boast the highest labor force participation rate among all archetypes at 59.8% and lead in overall resident well-being.

- Manufacturing Workshops: Accounting for 26% of the rural population, these are hubs where manufacturing represents 30% or more of GDP. These regions offer the strongest opportunities for upward economic mobility for middle-income residents.

- Resource-Rich Regions: These small, remote communities specialize in resource extraction (mining, oil, and gas), which accounts for over 25% of their GDP. While they face industrial shifts, they generate twice the GDP per capita of agricultural powerhouses.

Strategic Alignment: Promised Land and Rural OZ 2.0

The McKinsey thesis provides a clear roadmap for the next generation of place-based investing. The Promised Land Opportunity Zone (PLOZ) strategy aligns directly with the McKinsey strategic findings, leveraging the Opportunity Zone 2.0 (OZ 2.0) framework established under the One Big Beautiful Bill Act (OBBBA) in July, 2025.

Core Farmland Strategy

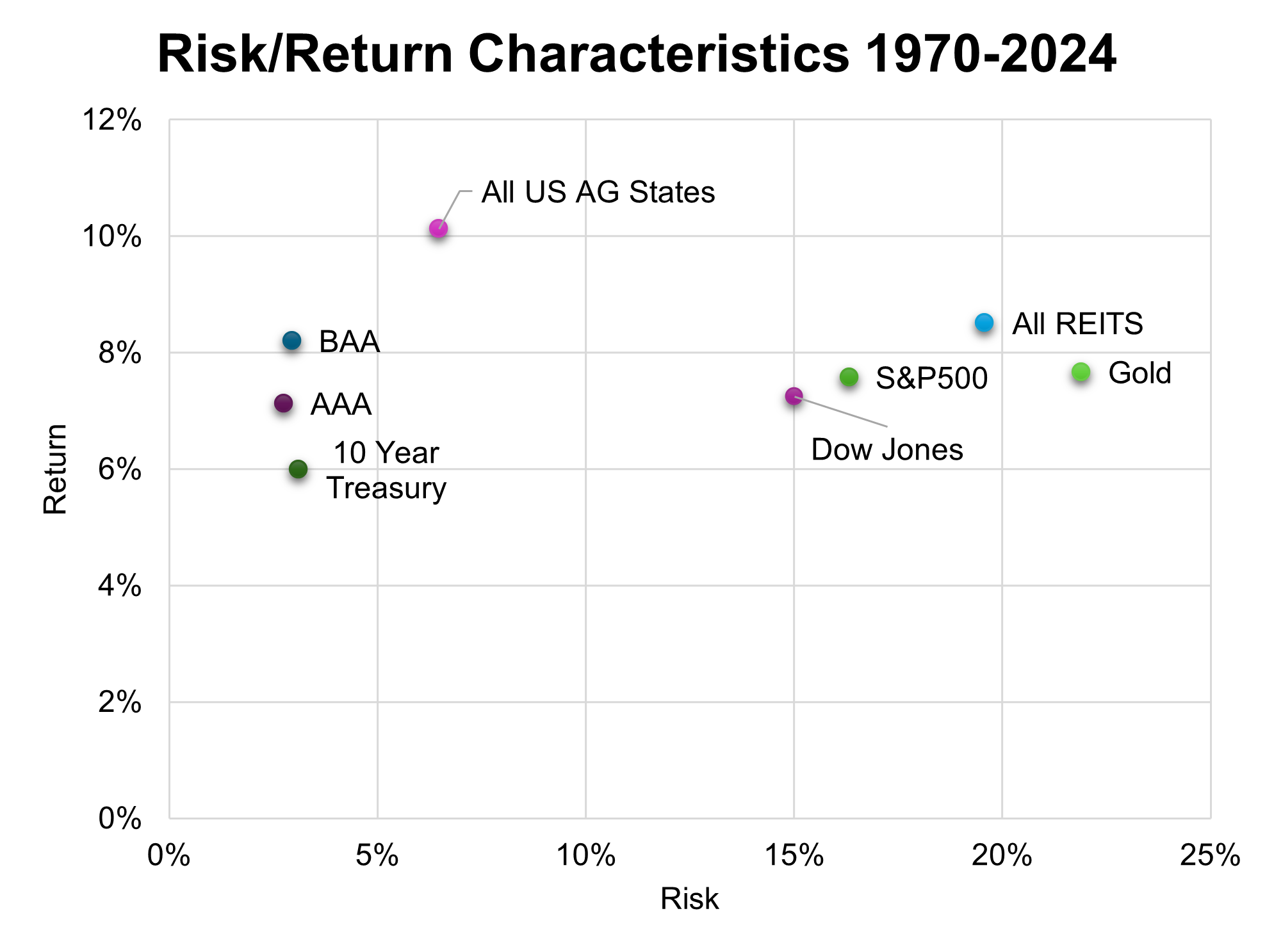

Promised Land’s foundation is built on investing in and improving high-quality US farmland located in OZs — the backbone of the "Agricultural Powerhouse" archetype. Farmland has historically provided superior risk-adjusted returns compared to traditional assets like the S&P 500 or Gold.

| Source: TIAA Center for Farmland Research |

Under OZ 2.0, the introduction of Qualified Rural Opportunity Funds (QROFs) significantly enhances the appeal of these investments:

- 30% Basis Step-Up: QROF investments receive a 30% basis increase after five years, compared to 10% for standard funds.

- Lower Improvement Threshold: The "substantial improvement" requirement for rural OZs is reduced from 100% to 50%, facilitating easier entry for projects like large-scale drainage tiling and grain storage.

Downstream: Qualified Production Activities

Beyond the soil, Promised Land sees considerable potential downstream of the farm in Qualified Production Properties (QPP). Under the OBBBA, QPP incentives can be applied to the "substantial transformation" of agricultural products. Examples include:

- Dairy Milking and Processing Parlors

- Grain Milling or Processing Plants

- Poultry Slaughter and Beef Packing Houses

An Opportunistic Frontier: Critical Minerals

Further afield of the agricultural sector, where we might apply a more opportunistic approach is the "Resource-Rich" real assets that are required to power modern economic activity, such as lithium, rare earth elements, and Dr. Copper. McKinsey identifies resource-rich regions as ideal for specialized mining growth, such as Missouri's tech hub for critical minerals processing, which is projected to create $34 billion in economic value.

By combining rural OZ tax benefits with a strategic focus on critical minerals—as explored in Servant Financial’s recent blog series—investors can target the "chokeholds" of the global supply chain, turning remote rural areas into potentially vital pillars of national security. Some of these resource rich rural OZs may have a common feature like Winslow, Arizona, a rail line and station.

Winslow Station is a historic railroad depot located at 303 East Second Street in Winslow, Arizona, serving as the primary Amtrak stop for the city and an integral part of the adjacent La Posada Hotel complex, which together form a key landmark along former U.S. Route 66. Winslow station serves as a flag stop on Amtrak's Southwest Chief route, operating daily between Chicago, Illinois, and Los Angeles, California, providing eastbound and westbound service to connect passengers across the Midwest, Southwest, and West Coast. Freight traffic over the years centered on lumber from northeastern Arizona forests, such as Ponderosa Pines, and livestock shipments, including cattle and sheep from Navajo County ranches.

The Winslow station's prominence in popular culture stems from the 1972 Eagles song "Take It Easy," which famously includes the lyrics "standin' on a corner in Winslow, Arizona." Although the song references a street corner rather than the station itself, it captures the many rural American towns’ quintessential rail, agricultural, manufacturing, and mineral resource heritage and that laid-back vibe and peace of mind often found on main street.

Resources:

Author: John Heneghan

The American Heartland is standing at the threshold of a historic rural investment boom. With the passage of the One Big Beautiful Bill Act (OBBBA), Opportunity Zone 2.0 is no longer just a concept—it is a high, precision GPS-guided, 48-row planter behind a 500-horsepower tractor sowing seeds for the next great rural American renaissance. At Promised Land, we aren't just sitting idly by waiting for the OZ map to change; we are preparing for more favorable weather and an expected optimal investment climate ahead for rural OZs. We are aligning investor capital with the abundant, fertile growing regions across the country to ensure that American farming communities remain a vibrant backbone of our national economy.

Opportunity Zone 2.0 is in the early stages of its program rollout and Promised Land OZ is well-positioned to lead the educational and community engagement aspects. As we mentioned in our blog post, OZ 2.0 Takes Aim at Rural America, the Opportunity Zone Program was extended under the OBBBA on July 4th, 2025. The program extension establishes a permanent framework for opportunity zone investment with special incentives for investments in rural opportunity zones. While standard, non-rural Opportunity Zones offer a 10% step-up after a mandatory 5-year capital gain deferral period, the OBBBA has been designed to supercharge rural OZ investment. By offering a 30% step-up in basis, the federal government isn't just inviting investment—it’s issuing a mandate for revitalization of the American Heartland.

States and Federal Government Timeline

As the State Governors and the U.S. Treasury begin working through the OZ tract designation and certification process for Opportunity Zone 2.0, Promised Land is preparing to seed the next generation of rural growth by efficiently deploying investor capital at the program’s kickoff on January 1, 2027. Promised Land has a consistent track record of effectively deploying capital in farmland located in rural OZ communities. As the next generation of designations approaches, we are taking a proactive approach to ensure we are ready to move quickly to invest in farmland located in existing OZ 1.0 tracts and the OZ 2.0 cohort once these new tracts are finalized. Both OZ 1.0 and OZ 2.0 designated tracts qualifying as “rural” will be eligible for the 30% step up benefit.

From the timeline outlined below, state governors are quickly approaching their 90-day window to submit tracts for OZ 2.0 designation. Promised Land has been working to be an integral partner to this process in several states. Our fund manager, John Heneghan, accepted a seat on the Illinois Department of Commerce and Economic Opportunity (DCEO)’s Opportunity Zone 2.0 Ad Hoc Advisory Board. This actively positions Promised Land to continue its legacy as the leading rural development partner for Opportunity Zones located in American Farming Communities.

Activating the Pipeline for Rapid Deployment in 2027

In advance of the U.S. Treasury’s expected certification of new Opportunity Zone tracts, Promised Land is focused on expanding our sourcing network and deal pipeline to facilitate the rapid deployment of investor capital in 2027.

This includes engaging with potential partners, operating tenants, and prospective Fund III investors, while continuing to educate the broader investment community about the role Opportunity Zones can play in supporting agricultural land stewardship and rural economic development.

In January 2026, the Promised Land team presented during a breakout session at the Land Investment Expo in Des Moines, where we shared insights on Opportunity Zone 2.0 and its enhanced benefits for rural communities. In addition, John Heneghan attended the Novogradac Opportunity Zones Summit in December, delivering a similar presentation tailored to an investor-focused audience and highlighting how capital can be deployed effectively in rural Opportunity Zones.

Promised Land is also exploring other avenues to connect with our rural partners, such as attending the annual meeting of the Mid-South Chapter of American Society of Farm Managers and Rural Appraisers, and potentially sponsoring the 2027 FARMCON Conference hosted by Kevin Van Trump. Promised Land hopes to deepen its engagement with farmers who may have capital gains to reinvest, demonstrating how Opportunity Zone investing could provide a strategic way to put those gains to work.

At the same time, Promised Land is expanding its network of landowners, operators, and capital partners across agricultural regions. Through these relationships, the firm is identifying and pre-qualifying farmland assets that may fall within anticipated Opportunity Zone 2.0 boundaries. Our property pre-qualification strategy is discussed below. Preliminary diligence, property screening, and market analysis are being conducted to build a pipeline of potential acquisitions ahead of the designation deadline.

Post–November 28, 2026: Promised Land Deployment and Acquisition

Following the certification of updated Opportunity Zone designations by the U.S. Treasury, Promised Land will move to finalize property selections located within qualifying OZ 1.0 and 2.0 tracts.

With its acquisition pipeline flowing, the firm will advance full underwriting, finalize due diligence, negotiate, and execute purchase agreements on the most attractive farmland investments. The goal is to close on the highest priority farms in early 2027, positioning investors to benefit from OZ 2.0 program’s enhanced rural incentives, including the rolling deferral structure, 30% step up, and lower improvement requirements (50% versus 100%) for rural OZs.

Through this phased approach, Promised Land aims to remain at the forefront of rural Opportunity Zone investment, deploying patient capital into American farming communities while advancing long-term land stewardship practices and agricultural productivity.

Promised Land’s Pre-Qualification Strategy

To move at the speed of the market, we’ve standardized our vetting process to achieve two critical goals: education and execution. First, prequalification guidance will help educate the broader agricultural and investment community about the applicability of Opportunity Zones to farmland. Second, this guidance provides our partners with a practical framework for evaluating farmland properties and their suitability for OZ improvement requirements before presenting them to the Promised Land team.

The checklist allows partners to evaluate properties as they come to market and organize key information before submitting opportunities for underwriting review and valuation.

We’ve distilled years of institutional expertise into a streamlined 15-minute diagnostic. This isn't just a form; it’s the quickest path for our partners to move a 'potential lead' to 'actionable asset' before the ink on the Treasury's new maps even has a chance to dry. The checklist includes sections covering a property overview, Opportunity Zone qualification, potential development opportunities, a snapshot of the surrounding local economy, physical and soil characteristics of the cropland, and the qualifications and track record of existing tenant operator. Our hope is that this process empowers our partners to efficiently evaluate potential opportunities and forward the most promising properties to the Promised Land team.

The Property Overview section captures the basic information about the asset, including its location, asking price, acreage, and primary crops grown. We also ask partners to indicate whether they have an existing relationship with the property, whether through local familiarity, prior operating experience, or current management responsibilities.

The next section evaluates whether the property’s location qualifies under either Opportunity Zone 1.0 or Opportunity Zone 2.0. The existing Opportunity Zone 1.0 designations have been in place for several years, while the updated 2.0 designations are currently in development and expected to be released later this year. Fortunately, organizations such as Economic Innovation Group and Novogradac have developed tools that help determine whether a tract is likely to qualify under the updated Opportunity Zone 2.0 eligibility guidelines.

The central objective of the Opportunity Zone program is to drive private investment into lower income communities and census tracts that are starved for economic development. For farmland assets to align with both the program’s goals and Promised Land’s investment philosophy, properties must present a clear value-add improvement opportunity. Examples may include installing drainage tile, expanding or adding new grain storage capacity, adding irrigation systems, or making other capital improvements that increase the land’s productivity capacity and long-term value. Our partners, who often have deep local knowledge, are frequently better positioned to evaluate many of these development opportunities. Additional sections of the form ask partners to document a farm’s existing improvements and soil characteristics to help establish the property’s baseline condition for valuation purposes and determining whether further investment may be warranted and economically beneficial to farmer tenants.

Another important component of the evaluation process is the local economic environment of the property. Farmland located near key delivery points, such as export facilities, processing plants, or major crop offtake centers, often benefit from stronger long-term demand and logistical advantages. Our partners assess each property’s proximity to these critical infrastructure assets, along with general observations about the local agricultural economy, depth of potential tenant base, and competitive dynamics within the market.

The Path Forward

The Promised Land team is currently sharing this pre-qualification framework with its partnership network while educating the broader economic development community about the role Opportunity Zones can play in farmland investment. By combining a disciplined screening process with strong on-the-ground partnerships in these communities, Promised Land is building a scalable process aligned with the economic development goals of the Opportunity Zone program and the long-term benefits of committed stewardship of productive agricultural land.

Just as a 500-horsepower tractor prepares the field for a bountiful harvest, Promised Land is laying the groundwork for a new era of rural prosperity. As OZ 2.0 takes root, we remain committed to our mission: channeling patient, purposeful capital into the heart of rural America. Together with our partners, we are cultivating a legacy of responsible stewardship and robust economic growth that will sustain the American Heartland for generations.

Article By: Ailie Elmore

The 19th annual Land Investment Expo took place January 12–13 in Des Moines, Iowa, hosted by Peoples Company. The Promised Land team had the pleasure of both attending and presenting during one of the breakout sessions. The two-day event featured a Farmland Master Class on January 12, followed by dynamic presentations on January 13 from world-class economists, investors, farmers, agribusiness professionals, and other subject matter experts. Attendees represented a diverse range of backgrounds, including wealth managers, investment advisors, production agriculture professionals (farmers, ranchers, and vintners), land management and acquisition specialists, and educators. Sessions challenged listeners while offering a wide breadth of content, ranging from land values and returns to tariff disputes and sustainable farming practices.

Geopolitical strategy expert Peter Zeihan kicked off the conference with his presentation, “And Here We Are… At the End of the World.” Despite the ominous title, his commentary was not entirely negative, and his humor brought levity that even the most serious attendees could appreciate. A frequent Land Expo speaker, Zeihan is particularly adept at connecting global demographic trends and geopolitical events to their implications for the U.S. agricultural economy.

Much of his presentation focused on global population dynamics, including birth rates and aging trends, and how these factors influence economic growth, technological advancement, and infrastructure. China was a major point of emphasis, as the country faces a significant demographic challenge. Its one-child policy, in effect from 1979 to 2016, was implemented to curb what the government viewed as unsustainable population growth. However, the policy also led to unintended consequences, including a rapidly aging population and a severe gender imbalance, as cultural preferences for male children resulted in the widespread underreporting or abandonment of female births. Today, China faces a shrinking workforce and a surplus of working-age men with limited prospects for marriage and family formation. According to Zeihan, these demographic shifts pose serious challenges for China’s labor supply and threaten its long-term position as a global economic powerhouse.

Zeihan then turned his attention to the United States, discussing both demographic trends and the current political landscape. He noted that a wave of executive orders issued by President Trump reflects, in part, Congress’s ongoing difficulty in reaching decisions. Zeihan argued that globalization was always destined to fracture and that Trump merely accelerated this process. He also touched on the USDA’s challenges in implementing effective policy amid organizational strain and staffing shortages following recent federal employment cuts. These remarks served as a fitting introduction to the next speaker, USDA Deputy Secretary Stephen Vaden.

Vaden took the stage and responded directly to several of Zeihan’s comments regarding USDA inefficiency. He emphasized that the USDA is actively working to reduce its physical footprint while strengthening its capacity as an institution critical to farm economics. Vaden highlighted the agency’s ability to cut approximately $1 billion from its $203 billion budget by closing underutilized and vacant USDA buildings on the National Mall and across the country.

He also discussed plans to shift USDA operations away from Washington, D.C., and closer to its primary stakeholders, farmers. The USDA already maintains a significant presence in Kansas City, where the Economic Research Service is headquartered, making it a likely hub for expanded operations.

Vaden further referenced upcoming ad hoc support payments totaling $12 billion, expected to be distributed in February, to help farmers navigate a low commodity price environment driven by tariffs and strong crop yields and production. While the U.S. and China have reached an interim agreement and China has resumed purchasing soybeans at agreed-upon levels, uncertainty remains regarding the durability of current trade arrangements. In addition, there is ongoing discussion in Congress about potential supplemental legislation to provide additional assistance to farmers if market conditions remain weak. However, until such legislation is passed and funded, it remains unclear whether the USDA will be able to continue providing ad hoc support at similar levels in the future.

Following the morning keynote, the first round of breakout sessions began. Promised Land presented “Opportunity Zone 2.0 Goes Rural,” which explored updates to the Opportunity Zone Program included in the “One Big Beautiful Bill.” Led by John Heneghan and Mark Jablonski, the session highlighted the overall success of the initial Opportunity Zone program and outlined key program changes, with particular emphasis on new incentives designed to promote greater investment in rural Opportunity Zones and Qualified Production Properties (QPP). The presentation is available here.

The lunch keynote session featured a mix of award presentations, a discussion on family office involvement in agriculture, and a dose of what was affectionately described as “lunatic farming.” Peoples Company awarded its Farmer of the Year honor to Kevin Babb of Champaign County, Illinois, recognizing his lifelong achievements in agriculture.

Eric O’Keefe, master of ceremonies and editor of The Land Report, unveiled the Winter 2025 issue, which highlighted Stan Kroenke’s acquisition of nearly one million acres. The 937,000-acre purchase in New Mexico represents the largest single land acquisition in the United States in more than a decade and propelled the Los Angeles Rams owner to the top spot among U.S. landowners.

Following the unveiling, Joel Salatin took the stage and energized the room with his self-described “lunatic farming” philosophy. The prolific author and co-owner of his family farm described himself as a “Christian libertarian environmentalist capitalist lunatic farmer.” His operation provides meat and forestry products to more than 5,000 families, 10 restaurants, and five retail outlets. Salatin is also widely known for mentoring young people and advocating for local, regenerative food and farming systems.

Ron Diamond followed with a highly anticipated session titled “What Is a Family Office and Why Does It Matter?” Diamond, Founder and Chairman of Diamond Wealth, leads a syndicate of more than 100 family offices ranging in size from $250 million to $30 billion. He discussed how high-net-worth individuals are increasingly allocating capital to alternative assets, including farmland, and explored the evolving role of family offices in today’s investment landscape.

Diamond highlighted the massive generational wealth transfer underway, noting that approximately $124 trillion is expected to move from baby boomers to the next generation. As family offices grow in scale and sophistication, they are beginning to compete with, and in some cases encroach upon, traditional private equity. Unlike private equity firms, family offices typically operate with longer investment horizons, a tax-aware approach, and a patient-capital mindset with closely aligned interests.

He emphasized farmland’s ability to support long-term, multigenerational wealth objectives, aligning naturally with the perspective of family offices. Beyond financial returns, Diamond noted a growing desire among family offices to be part of America’s agricultural legacy, viewing farmland not only as a durable asset class, but also as a means of preserving land, supporting food production, and remaining connected to the country’s agricultural heritage. He concluded by posing a central question: “How do the rich people find the smart people, and how do the smart people find the rich people?”

The afternoon breakout sessions covered a wide range of topics, including timberland investment opportunities, farmland market overviews, water management strategies, succession planning, agricultural economics updates, and tax-deferred land strategies. The Promised Land team valued the opportunity to network with other professionals and explore potential collaborations during these sessions.

The afternoon keynote featured Ed Yardeni, President of Yardeni Research, Inc., who shared his outlook on the economy. He characterized the current decade as one of continued economic expansion, describing the U.S. as already six years into what he calls the “Roaring 2020s.” Looking ahead, Yardeni expressed confidence that growth will persist through the remainder of the decade and stated that he does not anticipate a recession in the near term.

Yardeni also addressed the intersection of politics and markets, cautioning investors against allowing political views to interfere with sound investment decisions. He emphasized that opportunities exist regardless of which party occupies the White House, noting that market downturns often present buying opportunities rather than reasons to retreat.

Geopolitical expert Marko Papic closed the expo with a forward-looking presentation titled “The End of U.S. Exceptionalism.” Papic suggested that 2026 will be shaped less by headline geopolitical events and more by economic policy decisions aimed at extending the current cycle. He highlighted the growing role of household wealth, particularly home equity, in sustaining economic momentum.

Papic also noted increasing investor interest in tangible, real assets such as land and minerals, suggesting that this shift should support long-term values. He expressed confidence in the stability of land and real estate markets over the coming decade, stating that he does not anticipate a meaningful change in their trajectory. Papic concluded by suggesting that land values may ultimately rival traditional stores of value, including gold, as investors continue to seek durable, inflation-resistant assets.

The Land Investment Expo 2026 reinforced the increasingly central role that land, agriculture, and real assets play in a rapidly evolving economic and geopolitical landscape. From global demographic shifts and domestic policy challenges to generational wealth transfer and long-term investment strategies, the conference underscored the importance of taking a broad, forward-looking view of agriculture and land ownership. Speakers consistently emphasized resilience, whether through farmland’s durability as an asset class, regenerative farming practices, or patient, values-driven investment, and highlighted the need for adaptability in an era of uncertainty.

For the Promised Land team, the expo offered valuable insights, meaningful dialogue, and opportunities to connect with like-minded professionals committed to the future of American agriculture. As investors, operators, and policymakers navigate the remainder of the decade, Land Investment Expo 2026 reemphasized farmland as a cornerstone of economic stability but also a lasting link to America’s agricultural heritage and long-term prosperity.

Author: Ailie Elmore

Introduction

Since its inception, the Opportunity Zone (OZ) program has mobilized nearly $100 billion in private capital, establishing itself as one of the most significant place-based economic development initiatives in the history of the United States. However, data from the Economic Innovation Group and the Joint Committee on Taxation indicates that the initial iteration of the program, OZ 1.0, saw investment flow disproportionately toward urban centers. While the program was successful in many regards, only an estimated 10% of total OZ capital reached rural low-income communities despite an estimated 40% of eligible tracts being considered rural in nature.

With the enactment of the One Big Beautiful Bill Act (OBBBA) on July 4, 2025, the landscape has shifted significantly. This legislation not only codified the Opportunity Zone program as a permanent economic tool but also introduced specific, powerful incentives designed to correct the previous urban-rural capital imbalance. By creating a distinct category and related incentives for rural OZ investment—the Qualified Rural Opportunity Fund (QROF)—policymakers have effectively widened the path for capital to flow into America’s agricultural heartland. For tax practitioners and investors, understanding the mechanics of these new rural-specific incentives is essential for planning future capital deployment.

A Permanent Framework for Investment

The most fundamental change introduced by the new legislation is permanency. The original program was a temporary incentive scheduled to sunset, but the OBBBA has transitioned the OZ regime into a permanent fixture of the tax code.

Under this new "OZ 2.0" framework, the investment period officially begins on January 1, 2027. This reboot comes with a new map; governors in all 50 states must submit new census tract nominations by July 2026. While the general structure of deferring capital gains remains, the legislation introduces a bifurcation in benefits that heavily favors rural investment.

The Qualified Rural Opportunity Fund (QROF)

To access the enhanced rural benefits, investors must utilize a Qualified Rural Opportunity Fund (QROF). The legislation defines a QROF as a fund that invests at least 90% of its assets into designated "rural OZs." This distinction is critical. A standard Qualified Opportunity Fund (QOF) continues to offer attractive tax efficiency, but a QROF unlocks two specific "super-incentives" designed to effect change in rural economies: a significantly higher step-up in basis and a lower substantial improvement threshold.

Rural America’s Fundamental Case: Food, Fuel, and Fiber

While tax incentives provide the catalyst for capital movement, the underlying investment thesis for rural Opportunity Zones rests on its production of essential resources. Rural economies are generally anchored around the production of the necessities of life: food, fuel, and fiber. Because demand for these commodities is constant, the asset classes associated with their production—specifically cropland, pastureland, and agricultural facilities—have historically demonstrated unique economic resilience.

Data courtesy of the TIAA Center for Farmland Research at the University of Illinois covering the period from 1970 to 2024 highlights this attractive risk-reward profile. During this timeframe, farmland delivered equity-like returns of approximately 10% (outperforming the S&P 500 of approximately 8%) yet maintained a lower risk profile than the S&P 500 that was more comparable to bonds, with volatility near 7%. The underlying historical performance data suggests that rural assets can function as an inflation hedge similar to gold, but with the distinct advantage of generating annual operating income—effectively acting as a store of value with a "coupon."

[This Risk/Return Graphic is based on data from the TIAA Center for Farmland Research (1970–2024), farmland occupies a unique investment quadrant: offering equity-like returns (~10%) with the low volatility profile of fixed income (~7%).]

This stability is particularly relevant to the Opportunity Zone structure, which mandates a long-term hold. Historical performance indicates that farmland values appreciate at a spread of roughly 2% over inflation. Furthermore, the historical data shows that investors who held farmland for the 10-year period required by OZ rules would have remained in positive territory, even if they had purchased at market peaks preceding major economic downturns like the 1980s farm crisis. By coupling these fundamental attributes with the new OZ 2.0 incentives, the rural sector presents a compelling case for risk-aware, long-term capital.

Supercharged Incentive #1: The 30% Step-Up

The first, and perhaps most attractive, incentive for investors is the enhanced step-up in basis. Under the standard OZ 2.0 rules, an investor who holds their interest in a QOF for five years receives a 10% step-up in basis on the deferred taxes. This is a valuable benefit, effectively reducing the tax liability on the original capital gain by 10%.

However, the OBBBA provisions state that for investments made through a QROF, that benefit triples. Investors who hold their QROF investment for five years receive a 30% step-up in basis. This dramatic increase significantly alters the return profile for rural investments, offering a "buffer" that can make rural development deals competitive with potentially higher-yielding urban real estate development projects. This 30% step-up acts as a powerful

magnet for patient capital, rewarding investors for allocating capital to rural areas that have historically struggled to attract institutional capital.

Supercharged Incentive #2: The 50% Improvement Threshold

The second hurdle in the original OZ program was the "substantial improvement" requirement. To qualify for tax benefits, an investor purchasing an existing asset generally had to double its basis—investing $1 for every $1 of the asset’s value (excluding land) within a 30-month window. In rural settings, where asset values can be idiosyncratic and construction logistics more challenging, this 100% improvement threshold often proved challenging.

The new legislation directly addresses this potential impediment. For QROFs, the substantial improvement requirement is reduced to 50% of the property's acquisition basis (excluding land).

This lower threshold is a game-changer for agricultural operations, making a wider range of infrastructure upgrades economically viable. For example, a farming operation might not need to double the value of its existing improvements to increase the farm’s productivity. Under the new rules, a moderate investment in modernization of production facilities and farm equipment, such as grain bin storage, drainage and irrigation, now qualifies.

Practical Application: What Qualifies?

The OBBBA may also open the path for higher return seeking OZ investors to venture into downstream agricultural infrastructure. In addition to reauthorizing bonus depreciation on equipment with useful lives of 20 years or less, the OBBBA established similar accelerated depreciation on Qualified Production Property or QPP. Newly constructed facilities eligible for treatment as QPP would typically have IRS useful lives of 39 years, but if they meet the definition of QPP these assets can be fully depreciated in the year placed in service. QPP must be used for manufacturing, production, or refining activities. Eligible “production” activities under the OBBBA have been specifically limited to agricultural and chemical production. The legislation is also specific about what constitutes a qualified activity, focusing on the "substantial transformation" of personal property.

Practical examples of downstream agriculture infrastructure investments that could be feasible under the QROF structure include:

- Grain Milling: Facilities that process raw grain into feed or food products.

- Livestock Operations: Dairy milking parlors, poultry processing plants, and hog confinement facilities.

- Specialized Processing: Facilities for wool shearing, egg production, or aquaculture.

QPP within a QROF would offer a highly attractive investment for OZ investors while simultaneously modernizing the American heartland’s aging agricultural infrastructure.

Conclusion

The transition to Opportunity Zone 2.0 marks an important shift from a broad-brush approach to a more targeted economic strategy. By offering a 30% basis step-up and lowering the improvement barrier to 50%, the OBBBA acknowledges the unique economic realities of rural America. These incentives are likely to affect a meaningful movement of capital gains from traditional urban real estate into America’s breadbasket, offering investors tax efficiency while providing rural communities the opportunity to modernize agricultural infrastructure for the production of the necessities of modern life.

Article By: John Heneghan

The time has once again come for farmers across the United States to harvest their crops and bring another growing season to a close. If you’ve traveled through the I-States (Indiana, Illinois, or Iowa) recently, you’ve likely seen combines rolling steadily across fields, reaping what has been sown. Harvest time is both exhausting and deeply rewarding, a season that stirs memories of past years while sowing hope for what lies ahead.

Still, 2025 has not been an easy year for U.S. agriculture. Tariff tensions have weighed heavily on commodity markets, pushing prices below breakeven levels amidst uncertainty about end market demand and where this year’s grain will ultimately go. As of late October, December corn futures sit around $4.29 per bushel, and November soybeans near $10.64. According to the University of Illinois Farmdoc team, break-even prices for high-productivity farmland are closer to $4.63 for corn and $10.87 for soybeans, meaning most producers are operating in the red. Some farmers sold a portion of their crop when prices peaked in the spring, before tariff headlines hit in April, but most farmers have held back, hoping for a rally that has yet to materialize.

A recent Farm Journal survey of more than 1,100 corn producers signals that 2025 yields will likely fall short of 2024’s record output. The national average is expected to be near 178.5 bushels per acre, down slightly from last year’s 179.3. The steepest declines are showing up in the key I-states, with Illinois down about 7%, Indiana off 4.6%, and Iowa down 3.2%. In contrast, northern states like Minnesota and South Dakota are expected to post modest gains of roughly 3–4%. Disease pressure, late-season dry spells, and localized stress have been key challenges. As of mid-October, roughly 43% of the corn crop had been harvested, and 79% of soybeans were in the bin, helped along by favorable in field drying weather. Storage capacity, however, is becoming a pinch point in parts of the Northern Plains, where over half of South Dakota farmers reported insufficient space for this year’s crop. Even a modest national yield dip in the heart of the Corn Belt could have an outsized influence on overall production and pricing dynamics heading into the 2026 crop year.

Economically, many producers are feeling the squeeze. Farm economists warn that the current downturn is serious, but not quite a replay of the 1980s farm crisis. Nearly 70% of economists see parallels to that difficult decade, but they also note that today’s farmers benefit from stronger USDA safety nets, crop insurance programs, and credit frameworks. The headwinds are clear: soft global demand, high input costs, and continued consolidation across the ag sector. Livestock markets have remained relatively stable, but crop producers are bearing the brunt of compressed farming margins. Economists describe the situation as a “slow grind” rather than a collapse. The situation is painful for the ag sector, but with resiliency has been built into the sector over many trials. Recovery of farming margins will likely come slowly and unevenly.

Amid these challenges, the USDA’s announcement to release over $3 billion in farm aid offers some much-needed relief to stressed farmers. The funds, drawn from the Commodity Credit Corporation, had been frozen during the recent government shutdown. The government shutdown has also delayed USDA loan processing and farm-service payments at a critical time in the harvest cycle. This new round of support aims to help producers navigate low commodity prices, high input costs, and lingering trade disruptions. Still, questions remain about eligibility, timing, and whether more aid, potentially totaling $10 billion or more, may follow.

In short, the 2025 harvest tells a familiar story in American agriculture: resilience under pressure. Yields may be a touch lighter, the margins tighter, and the markets uncertain, but the hard work of the harvest continues. As combines finish their passes and grain bins fill, farmers across the country are once again doing what they’ve always done best, getting the crop in, steadying their balance sheets, and preparing to start all over again next spring.

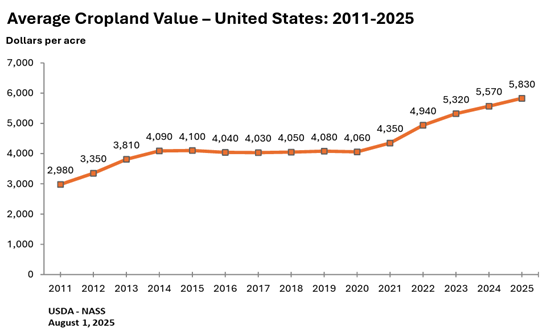

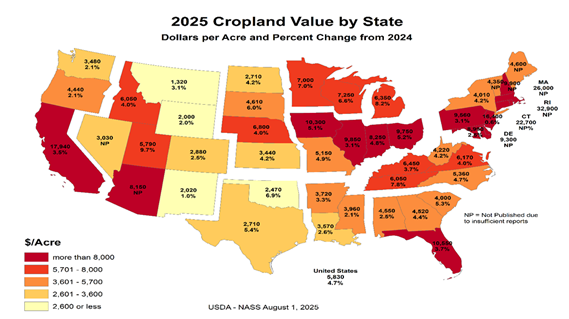

The month of August often signals a season of transition and excitement—back-to-school mania, the kickoff of college football, and the return of the ever-popular pumpkin spice latte at Starbucks. In agriculture, however, August also marks the release of one of the most anticipated publications of the year: the USDA Land Values Summary.

The USDA Land Values Summary is an annual report from the National Agricultural Statistics Service (NASS) that provides average values of U.S. farmland (farm real estate, cropland, and pastureland) and the average cash rental rates for cropland and pasture. It’s important because farmland is the foundation of U.S. agriculture, and its value is a key indicator of the health of the farm economy. Rising or falling land values affect:

- Farmers and landowners – influencing borrowing power, equity, and farm profitability.

- Investors and lenders – serving as a measure of asset strength and collateral value.

- Policy and research – guiding decisions on agricultural programs, conservation, and rural development.

In short, the summary provides a national “benchmark” for assessing farmland affordability, producer balance sheets, and broader rural economic conditions. Data are collected directly from producers through nationwide surveys, with results broken down by region and state. The report first presents farm real estate values (all agricultural land and buildings), and then provides more granular analysis by cropland and pasture categories.

For Promised Land’s purposes, our focus remains on cropland values, which most directly align with our investment strategy.

Current Trends in Cropland Values

Cropland values continue to trend upward across the United States, even as commodity prices have weakened throughout much of 2024 and 2025. Historically, land values have been closely correlated with commodity prices. Many agricultural stakeholders expected land values to decline this year in response to lower commodity prices, tariff concerns, and generally declining farm income. While lower-quality land has begun to see a leveling off in values, higher-quality land and land with development potential have continued to appreciate. Note that USDA uses Average Total Cropland meaning it includes both lower quality and higher qualities farmland in the calculation. Promised Land's focus is to invest in high quality, very productive farmland meaning these averages are not reflective of the quality of Promised Land's portfolio.

At the state level, we see the familiar pattern of strong average land values in the Corn Belt, California, and Florida—some of the most agriculturally productive regions in the country. Although these states are no longer experiencing the near double-digit growth that followed the COVID-19 pandemic, they remain resilient and continue to demonstrate strength in a challenging agricultural environment

Concerns remain, however, that these trends may not be sustainable. Tariffs continue to take effect, demand for solar and wind projects is slowing, and commodity prices lack momentum. The USDA has already revised its harvest yield expectations upward by 7.8 bushels in the August 2025 Crop Production Report compared to July’s report. Ideal growing conditions in Iowa, Nebraska, and parts of Illinois and Indiana are contributing to expectations of a large harvest, which could further depress commodity prices. As farmers move into harvest season, the global agricultural community will be monitoring these reports closely.

As Promised Land continues to develop plans for OZ 2.0, our efforts will remain concentrated in areas of the country that have demonstrated strong growth in land values and continue to show promise for future expansion.

Perhaps the apex of economic fireworks this summer came with the passage of the "One Big Beautiful Bill" (OBBB) —a key campaign promise from President Donald Trump. At the start of the season, there was some uncertainty expressed by media and political pundits whether the legislation would reach the Resolute Desk before summer’s end. However, on July 4th, President Trump officially signed the bill into law.

This landmark legislation builds on one of the signature achievements of Trump’s first term: the 2017 Tax Cuts and Jobs Act, which originally created the Opportunity Zone (OZ) program. The new bill makes the OZ program permanent, with a range of significant updates and modifications. While the whole OBBB legislation spans 887 pages and addresses numerous government revenue and spending provisions, our focus here is on the changes to the Opportunity Zone program.

Extension and Redesignation of the Opportunity Zone Program

The current investment period of Opportunity Zones 1.0 is set to expire on December 31, 2026. A new investment and gain deferral period (OZ 2.0) will begin on January 1, 2027, and importantly includes special incentives for rural revitalization. OZ 2.0 establishes rolling 5-year capital gain deferral periods and rolling 10-year holding periods from the date of the investment into a qualified opportunity zone fund (QOF) with redesignation of OZs every 10-year anniversary of January 1, 2027.

Under the updated framework:

- The governors of each state must submit new census tracts for OZ 2.0 designation, but only up to 25% of their eligible low-income tracts.

- States must submit their tract nominations by July 2026 to the U.S Treasury Department, with new OZ designations expected to be announced shortly thereafter.

It’s important to note: this new program does not renew the OZ tracts designated under the existing OZ 1.0 program. The tax deferral benefits under the original OZ framework will expire on December 31, 2026 and such gains deferred under OZ 1.0 will largely become taxable. No further OZ 1.0 investments can be made in the original zones after this date. However, existing OZ census tracts will remain in place for tracking and reporting purposes, particularly as it relates to the 10-year holding requirement for tax free capital gain treatment upon exit.

Promised Land has successfully completed all capital improvement requirements on the farms within its Fund I portfolio and has been closed for new investment since 2022, positioning us well for this OZ transition phase.

Tightened OZ Eligibility Criteria

The OZ 2.0 program narrows the definition of a "low-income community" to more narrowly target economically distressed areas. A census tract must now meet one of the following conditions:

- A poverty rate of at least 20%, or

- A median family income not exceeding 70% of the area median income (AMI).

Additionally, tracts where the median family income exceeds 125% of the state or metropolitan median are excluded from eligibility. These changes are intended to ensure that investment flows only to underserved regions.

Tax Incentives and Benefits

The OZ 2.0 is particularly attractive for investments in rural America, thanks to key tax benefits:

- Capital gains invested in a qualified opportunity zone fund (QOF) or QROF after December 31, 2026 may be deferred and recognized 5 years after the date of investment.

- Basis step-ups are enhanced:

- Investments in the QOF receive a 10% basis increase after five years.

- Investments in Qualified Rural Opportunity Funds (QROFs) receive triple the tax benefit with a 30% basis step-up after five years.

- The gain exclusion after 10-year hold remains in place, allowing investors in both QOFs and QROFs to exclude gains from OZ investments held for at least a decade.

Eased “Substantial Improvement” Rules for QROFs

Under the original OZ rules, tangible property had to be “substantially improved”—typically by doubling its tax basis—for investors to qualify for OZ tax benefits. The new bill maintains the threshold for QOFs but lowers this threshold to 50% only for QROF, significantly reducing the barrier to entry for rural development projects.

More Transparency & Reporting

OBBB introduces robust reporting requirements to improve oversight and public confidence in the program. Both QOFs and QROFs must now submit annual reports detailing:

- Asset composition,

- Types of investments made,

- Job creation metrics,

- Census tracts where investments occurred.

Failure to comply carries stiff penalties—up to $50,000 per year for larger funds—highlighting a renewed emphasis on transparency, impact measurement, and program integrity.

For more details and expert analysis on OZ 2.0, we encourage you to consult the following resources:

Economic Innovation Group: https://eig.org/opportunity-zones-2-0-where-things-stand/

Supportive OBBB Provisions

There were a few additional provisions in the OBBB that appear to be very supportive of Promised Land OZ’s farmland and agricultural sector strategy that we’d like to briefly highlight for our readers.

The OBBB includes a Special Depreciation Allowance for Qualified Production Property. Think of this as the Build Baby Build provision. This OBBB provision allows an additional first-year depreciation deduction equal to 100% of the adjusted basis of “qualified production property (QPP).” Under prior law, owners of nonresidential real property had to depreciate the cost of such property over a 39-year period. A “qualified production activity” is defined in the OBBBA as manufacturing, production (e.g. agricultural production and chemical production) or refining of a “qualified product” which is generally defined as tangible personal property. Construction of QPP must begin between January 19, 2025, and January 1, 2029; and be placed in service before January 1, 2031.

There is also a OBBB provision that provides for a 25% interest exclusion for tax purposes on new loans by banks, insurance companies and savings associations to rural or agricultural real property. The term ‘rural or agricultural real estate’ means (A) any real property which is substantially used for the production of one or more agricultural products, (B) any real property which is substantially used in the trade or business of fishing or seafood processing, and (C) any aquaculture facility.

In addition, a new provision in the OBBB brings a meaningful tax deferral opportunity to farmers selling farmland to other farmers. Under Section 1062 of the bill, sellers of “qualified farmland property” to “qualified farmers” would be allowed to pay the capital gains tax from the sale in four equal annual installments. This is a significant shift from the current requirement to pay the full tax in the year of sale. This farmland gain deferral provision requires that the farmland buyer be contractually obligated to actively farm the property for 10 years which dovetails with QROF holding period requirements.

Promised Land’s Future

Promised Land is proud to have played a role in the rural revitalization made possible by the Opportunity Zone Program. We’ve proven our ability to execute farmland acquisitions and capital improvement projects under the current OZ framework. Promised Land OZ’s two prior funds would meet the new OZ 2.0 definition of a QROF. It is our intention for PLOZ Fund III to qualify as a QROF. Looking ahead, we are updating our offering materials to align with the new OZ 2.0 program rules. We expect to begin capital raising efforts and deal sourcing well in advance of the January 1, 2027 launch date so we can “get the plow in the ground” once the new tracts have been designated. Promised Land will conduct rigorous due diligence on rural properties to identify high-impact opportunities with attractive risk-adjusted returns for future investment.

If you’d like to stay informed about upcoming offerings and developments, we invite you to visit us at https://promisedland.fund.

From Farm to Future, Promised Land OZ is committed to being the leading rural development partner for Opportunity Zones located in American farming communities.

Washington, DC, May 8, 2025

Overview

The Opportunity Zone Summit, hosted on May 8, 2025, in Washington, DC, and sponsored by Great Opportunity Policy, a policy advocacy group, brought together policymakers, developers, and economic experts to celebrate the success of Opportunity Zones (OZs) and advocate for their legislative extension and expansion. Established under the 2017 Tax Cuts and Jobs Act (TCJA), Opportunity Zones (OZs) incentivize private investment in economically distressed communities through tax benefits, aligning with the Promised Land Opportunity Zone’s mission to deliver financial returns and social impact through strategic investments in rural agriculture.

(Photo Courtesy of Great Opportunity Policy)

Keynote Address: Senator Tim Scott

Senator Tim Scott, the “father” of OZ legislation, opened the summit with a compelling case for OZs as a pathway to the American Dream. He highlighted:

- $90 Billion in Investments: Private capital has driven disciplined, impactful projects in underserved communities.

- Talent and Opportunity: OZs unlock potential in areas often overlooked, emphasizing individual effort over geographic limitations.

- Permanency Proposal: Scott advocated making OZ tax incentives permanent to provide program certainty for investors, low-income communities, and businesses. Advocates suggested a continuous rolling 10-year period to alleviate program discontinuities.

- Rural Focus: Scott emphasized potentially enhanced provisions to address historically limited investment in rural communities, aligning with our firm’s focus on farmland and rural OZ projects.

Congressional Update: Senators Mike Crapo and Tim Scott

Senators Crapo and Scott outlined the legislative path forward for OZs, leveraging the Budget Reconciliation process to bypass potential Senate filibusters:

- TCJA Extension: The 2017 TCJA, which includes the OZ provisions, delivered a $1.5 trillion tax cut that Crapo claims paid for itself. Without renewal, its expiration could result in a $4.3 trillion tax increase, with individual and pass-through entities, like family and business partnerships, being the hardest hit.

- Permanency Benefits: Permanent OZ incentives would enhance business certainty and encourage investors to continuously recycle OZ gains in this impactful investment program, much the same as tax deferred 401(k)s and IRAs allow for continuous tax deferral until funds are withdrawn.

- Rural Investment Gaps: Scott highlighted the need for tailored policies to drive capital to rural OZs, reinforcing our firm’s commitment to agricultural communities. Crapo noted that OZs worked exceptionally well in his mostly rural state of Idaho, with 54% of state OZs attracting some level of investment.

- Synergistic Tools: The Senators noted broadly that Federal, state, and local policymakers need to better leverage other existing policy tools and incentives with OZ tax benefits.

Panel Discussions: OZ Impact and Opportunities

Panels provided data-driven insights and strategic opportunities for investors:

- Commercial Innovation & Opportunity Zones (Moderator: Emily Lavery; Panelists: Frantz Alphonse, John W. Lettieri, Ying McGuire, Yves M. Mombeleur):

- $90 Billion in Equity: This is a three-year-old figure, likely much higher now. This figure also does not include debt financing. Created 300,000 net new housing units (double prior levels) in OZs along with significant job creation.

- Supply Chain Resilience: Frantz Alphonse highlighted OZ's potential to support domestic supply chain businesses post-COVID, aligning with the Trump administration's priorities to reshore manufacturing and boost blue-collar employment opportunities.

- Community Alignment: Ying McGuire emphasized simplifying processes for minority-owned businesses, with 1,500 corporate members in her network, including Microsoft and Georgia Power, supporting OZ funds for affordable housing.

- Call for Permanency: Yves Mombeleur urged permanent OZ incentives to sustain private investors and community program confidence.

- Leveraging Policy for OZ Success (Speakers: Scott Turner, Ben Carson, Vince Haley; Moderator: Ja’Ron Smith):

- Public-Private Partnerships: Ben Carson underscored OZs as a model for collaboration, leveraging faith-based communities to drive social good for the most vulnerable Americans.

- Housing Impact: HUD Secretary Scott Turner reported 300,000 housing units built within OZs, including Miami’s Liberty Square ecosystem, integrating housing, education, and workforce training.

- State Flexibility: Vince Haley proposed allowing state governors to select OZs for targeted residential or commercial development and reforming land-use laws to streamline residential permitting and improve housing supply and affordability.

- Private Sector Investment: Real Estate Development (Speakers: Louis Dubin, Jonathan Goldstein, Michael R. Harris; Moderator: Jill Homan):

- Community Engagement: Harris stressed the need for better communication with OZ communities to build trust and maximize impact.

- Flexible Financing: Goldstein advocated for OZ structures that support operating businesses’ working capital needs, enhancing investment flexibility. He noted that a substantial portion of the $90 billion of OZ investment went into real estate businesses, rather than manufacturing, services, or other operating businesses.

- Addressing Gaps: Dubin highlighted demand for workforce and multi-generational housing, as well as healthcare infrastructure, offering opportunities for diversified portfolios for investors.

Policy and Economic Outlook: Sustaining OZ Growth

Economic and policy leaders outlined strategies to enhance OZ's viability:

- Kevin Hassett and Stephen Miran (Economic Policy Discussion):

- Economic Growth: Hassett, former Chairman of the Council of Economic Advisors, projected sustainable 3% GDP growth with TCJA and OZ permanency. He cited a rule of thumb that $1 trillion in additional Federal revenue is generated for each 1% increase in GDP.

- OZ as Equalizer: OZs address geographic inequality, modeled after Jack Kemp’s enterprise zones, with a private equity-style approach to capital recycling.

- Rural Prioritization: It was noted that House Ways & Means Committee Chairman Jason Smith is exploring special provisions for rural OZs, a welcome catalyst for our farmland-focused strategy.

- Lynn Patten (Fireside Chat, President Trump Staff Member):

- Trump’s Commitment: President Trump supports OZs, driven by fairness and merit-based opportunities. She noted little-known facts that Trump increased funding for Historically Black Colleges and Universities (HBCUs) and public housing in his first term.

- Community Focus: Patten highlighted Trump’s personal engagement with communities for East Palestine, OH, to Flint, MI, reinforcing OZ alignment and desired social impacts.

- Alex Smith (Department of Treasury - Community & Economic Development):

- Streamlined Capital Access: Treasury aims to facilitate OZ investments through financial education and public-private partnerships. She also mentioned a policy discussion for prioritizing rural communities.

- Efficient Investment Flow: Secretary Bessent is coordinating across agencies to ensure federal funds reach OZ projects efficiently, enhancing investor confidence.

In alignment with this momentum, the House of Representatives’ latest Budget Reconciliation effort—nicknamed the “One Big Beautiful Bill”—proposes significant enhancements to the Opportunity Zone program along with many other tax and spend budgetary items. A new round of OZ designations is set to take effect on January 1, 2027, featuring a tightened definition of low-income communities and a requirement that up to 33% of new zones be rural. While this increased rural focus is welcomed, the delayed start date may cause investors to hesitate until the new designations are active, and further delays could arise from the state-level selection process. To attract capital to these rural areas, the bill proposes a 30% basis step-up after a 5-year hold period and reduces the substantial improvement requirement from 100% to 50%. For OZ investments made after 2026, gains can now be deferred until December 31, 2033. A 10% basis step-up is available for assets in non-rural OZs held for five years, but unlike OZ 1.0, there is no 7-year benefit. Existing OZs will officially expire on December 31, 2026. The legislation also allows ordinary income to be deferred and receive the 10-year benefit, though it is not eligible for the 5-year basis step-up and is capped at $10,000 per taxpayer. The budget reconciliation provisions passed the House before Memorial Day weekend, and now the One Big Beautiful Bill will head to the Senate for further review and reconciliation. Many expect the Senate will rewrite the OZ section to at least address unintended timing considerations causing potential discontinuity in OZ investments.

Implications for Promised Land Opportunity Zone

The summit reinforces the transformative potential of OZs for low-income communities in rural and urban America:

- Proven Impact: With $90 billion in equity and 300,000 housing units, OZs have delivered measurable economic and social benefits, validating our investment thesis.

- Rural Opportunities: The repeated mentions by presenters of rural OZs and House drafting aligns with our farmland investment strategy, such as our 4,500-acre Pamlico County, NC, project and 858-acre Douglas County, IL, farm, where we leverage OZ tax benefits to enhance the productive capacity of the land while providing attractive risk-adjusted returns to investors.

- Permanency Prospects: Permanent OZ incentives would provide long-term certainty for investors and broaden our reach and impact on rural OZ communities. This enhancement is expected to be considered by the Senate.

- Diversified Portfolios: Opportunities in housing, healthcare, and supply chain businesses complement our agricultural focus with potentially many manufacturing, renewable energy, or minerals being cited in rural American communities.

- Policy Support: Treasury’s commitment to streamlining capital access and potential rural OZ enhancements signals a friendly environment for impact investors.

Next Steps

- Monitor Policy Developments: Track Budget Reconciliation process outcomes for TCJA and OZ's permanency and House legislative proposals for rural OZs through the Senate deliberation process.

- Engage Stakeholders: Engage public policy advocates around targeted rural OZ initiatives and redrafting by the Senate to address OZ investment discontinuity concerns.

- Expand Outreach: Strengthen community engagement in our OZ projects to build trust and align with local agricultural stakeholders.

Conclusion

The 2025 OZ Summit underscores the program’s overwhelming success and social impact on these communities, enthusiastic political support, and alignment with Promised Land Opportunity Zone’s mission. With strong policy support, a focus on rural communities, and proven investment outcomes, OZs remain a cornerstone of our differentiated farmland investment strategy. We invite existing and prospective investors to join us in capitalizing on opportunities to revitalize rural American communities while achieving attractive risk-adjusted returns.

For those looking for some visible passion for this blue collar and rural American comeback, please enjoy this Opportunity Zones - We’re Not Done Yet reel released by Great Opportunity Policy.

For more information, please contact us at info@promisedland.fund.